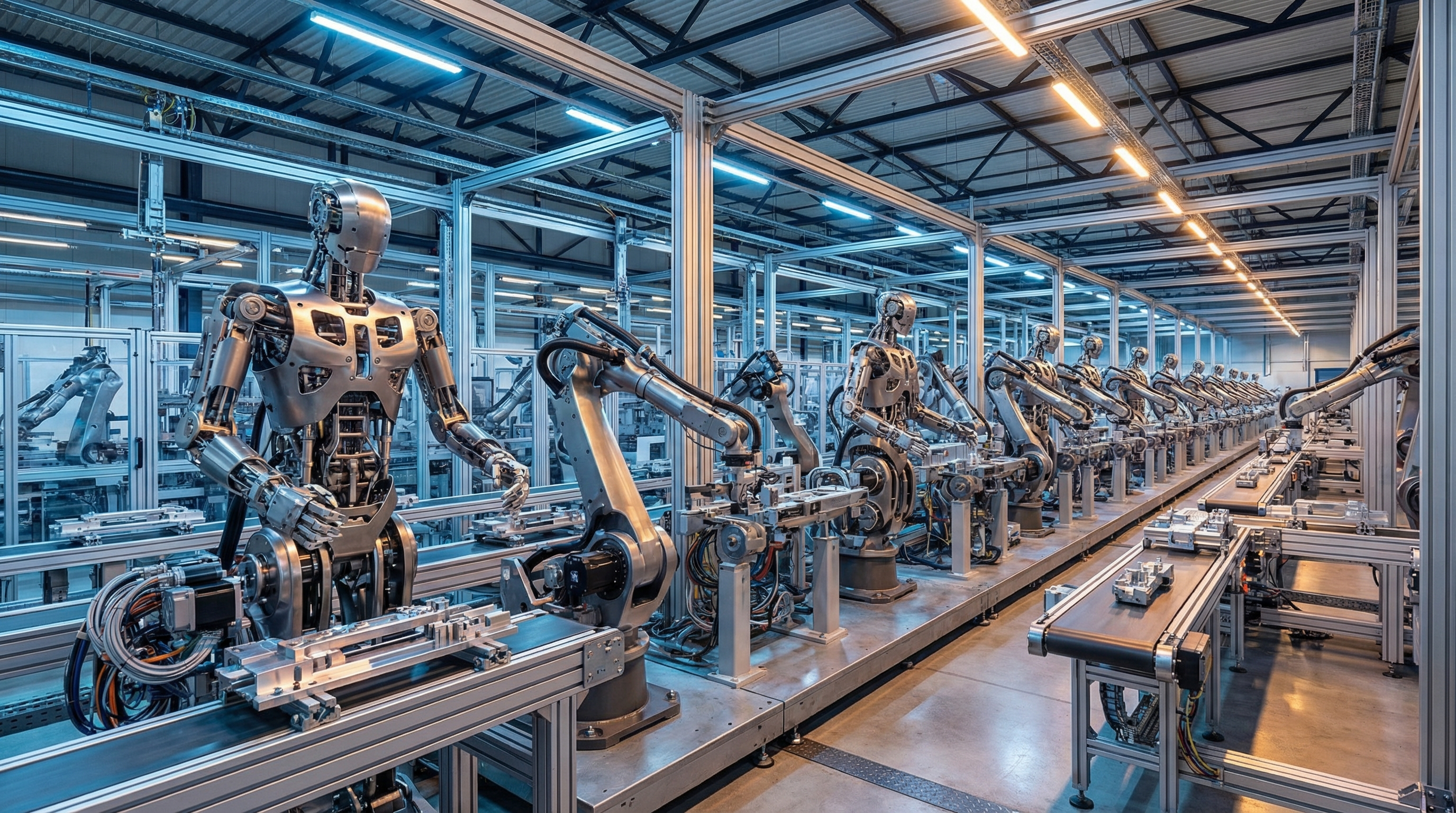

Tesla promised 50,000 Optimus robots in operation by the end of 2026. Agility Robotics opened a factory in Oregon capable of building 10,000 humanoids per year. Figure AI laid out a path to 100,000 units by 2029. Apptronik closed a $350 million Series A to scale production of its Apollo robot. Morgan Stanley analysts published a research note projecting a $5 trillion global market by 2050. The numbers were staggering. The investor excitement was real. Now it's late March 2026, Q1 is nearly over, and the question isn't whether the humanoid hype was warranted — it's whether the robots can actually do the job.

The Promises Were Specific. That's the Problem.

For years, robotics companies issued vague assurances about transformative impact "within the decade." By 2025, the industry had grown specific enough to be held accountable. Elon Musk told Tesla workers the company would produce at least 50,000 Optimus units in 2026. Agility Robotics, flush with funding and with its RoboFab facility now operating in Salem, Oregon, outlined production capacity exceeding 10,000 Digit robots per year. Figure stated there was a path to 100,000 robots by 2029. Apptronik, backed by Google and B Capital, raised $350 million in February 2025 to manufacture Apollo units for logistics and automotive customers including Mercedes-Benz and GXO Logistics.

Meanwhile, the analyst community piled on. Bank of America Global Research projected 18,000 humanoid robot shipments globally in 2025. Morgan Stanley Research estimated the total humanoid market would approach $5 trillion by 2050, with nearly one billion units in operation. Those are extraordinary projections. What they require is an equally extraordinary set of engineering and operational problems being solved — mostly at once, mostly in the next few years.

The hard part is that most of those problems haven't been solved yet. What follows is a clear-eyed examination of what's standing between the promise and the payoff.

Problem One: The Battery Math Doesn't Work for Industry Yet

Industrial environments run continuously. A factory floor doesn't pause for a 45-minute lunch break so the robots can recharge. Yet as of late 2025, Agility's Digit robot — one of the furthest-along commercial humanoids in actual deployment — operated on a 10:1 battery ratio: 90 minutes of total runtime, with 60 of those minutes reserved as buffer against unexpected pauses. That leaves a practical operating window of 30 minutes before recharge. The robot then needs 9 minutes to fully charge, which sounds fast until you're managing a fleet of 500 of them on a production line.

The deeper issue is reserve capacity. Humanoid robots in real factory settings frequently encounter unexpected situations: a misaligned part, a blocked path, a system waiting on an upstream process. Without a charge reserve, a robot that runs down mid-task in a logistics facility can require manual intervention — from a human who has to physically move more than 100 kilograms of inert robot. That's not just inconvenient. In a high-throughput facility running on tight margins, it's a deal-breaker.

Sleeker, thinner humanoid designs from competing companies are likely making compromises on battery capacity to achieve their form factors. The tradeoff between aesthetics and operational endurance is real — and industrial customers, who care very little how the robot looks, will punish it mercilessly.

Problem Two: The Reliability Bar Is Brutal

The humanoid robotics industry talks frequently about uptime. It talks less frequently about what industrial customers actually require. A factory operating at 99 percent reliability — widely considered excellent — will experience approximately five hours of downtime per month. When that downtime stops a production line, the cost can reach tens of thousands of dollars per minute. That's why automotive, electronics, and logistics customers typically expect 99.99 percent reliability from production equipment: two extra nines that represent less than an hour of annual downtime.

The gap between where humanoid robots are today and where industrial customers need them to be is not incremental — it's structural. Most humanoid deployments in 2025 were carefully controlled pilot programs: limited task ranges, supervised operation, hand-selected environments. Melonee Wise, who served as Chief Product Officer at Agility Robotics through late 2025, acknowledged in an interview with IEEE Spectrum that Agility had demonstrated 99.99 percent reliability in some specific applications — but not in the context of multipurpose or general-purpose functionality. The difference matters enormously, because multipurpose is exactly what the industry is selling.

Problem Three: Nobody Has Written the Safety Rules Yet

Before a humanoid robot can operate on an industrial floor in most jurisdictions, it needs to meet safety standards for machinery. Traditional industrial robots have well-established safety frameworks: safety cages, light curtains, emergency stop protocols. Humanoids, designed to work alongside people in shared spaces, don't fit neatly into those frameworks.

More concerning: the standard approach of simply cutting power when something goes wrong doesn't work for dynamically balancing legged robots. A bipedal machine that loses power mid-stride doesn't stand still — it falls. Potentially onto a coworker, a conveyor, or itself. Boston Dynamics is among the companies helping develop an ISO safety standard for dynamically balancing legged robots, with Agility and Figure participating. That standard is still being developed, meaning legal and regulatory frameworks for mass deployment are, at best, a moving target.

Matt Powers, Associate Director of Autonomy R&D at Boston Dynamics, put it plainly: the company intends to start with "relatively low-risk deployments" while building confidence in safety systems. A methodical approach, in his framing, is the winner. That's a reasonable position — but it sits in direct tension with the production timelines the industry has publicly committed to.

Problem Four: AI Won't Save You From Physics

The dominant narrative in humanoid robotics funding rounds is that advances in AI — particularly foundation models and large-scale training — will rapidly close the gap between prototype and production-ready robot. The logic draws a straight line from ChatGPT's emergence to general-purpose robotic intelligence, treating the latter as the inevitable downstream consequence of the former.

The robotics research community is considerably more skeptical. The core problem, as IEEE Spectrum's deep analysis of the field makes clear, is data: training a robot to generalize requires a scale of physical interaction data that simply doesn't exist yet. Text and image datasets for language models were collected passively over decades across the entire internet. Robotic manipulation data requires purposeful physical collection — robots doing things, in the real world, with feedback — and the available corpus is orders of magnitude smaller.

Google DeepMind's RT-2 and RT-X models demonstrated that training on large datasets yields promising generalization. But "promising" in a research context and "reliable enough for 99.99 percent uptime in automotive assembly" are not the same thing. As Wise noted, "a lot of people are hoping they're going to AI their way out of this. But currently AI is not robust enough to meet the requirements of the market." That assessment came from someone who had spent years watching humanoid AI up close.

The Form Factor Question Nobody Wants to Answer

There is a harder question underneath the production math: does a humanoid — specifically, a bipedal robot with arms — actually make sense for most industrial tasks? The intuition behind the humanoid form factor is that existing infrastructure was designed for humans: doorways, staircases, assembly lines, tools, storage racks. A robot shaped like a person can navigate that infrastructure without modification. That logic is real.

The operational reality is that most current humanoid deployments involve robots doing one thing, repetitively, on flat floors. They're not navigating stairs. They're not using human tools. They're moving boxes from one conveyor to another, or placing components in fixtures — tasks that wheeled robots with arms could do with greater reliability, at lower cost, and without the complex balancing dynamics that generate most of the technical risk. Agility's own Wise acknowledged the tension: "I don't think anyone has found an application for humanoids that would require several thousand robots per facility." If the practical advantages of bipedalism aren't needed for the actual work, the case for humanoid form factor narrows to long-term optionality — which is a valid investment thesis but a difficult near-term business model.

China's Supply Chain Advantage Is Growing

There is one dimension of the humanoid race that U.S. commentary underweights: China is building structural advantages in both deployment and supply chain that may prove decisive at scale. Morgan Stanley Research's May 2025 analysis projected China leading globally with 302 million humanoid units by 2050 — nearly four times the U.S. projection of 77.7 million. More immediately, China's national support for "embodied AI," as Morgan Stanley frames it, is driving capital formation at a pace that rivals have not matched.

The supply chain dependency runs deep. Nearly every humanoid robot developer in the world — including U.S. and European companies — relies on components sourced from China and Asia: screws, harmonic reducers, servo motors, and lithium batteries. As Morgan Stanley noted, "there are few U.S.-based alternatives for many humanoid components." Xiaomi's humanoid robot logged three consecutive hours of fully autonomous operation in a Beijing EV factory in early 2026 — an early but meaningful proof point. BMW and Hexagon's AEON deployment in Leipzig, which TTN covered in March, showed that European automotive can absorb humanoid robots — but it also illustrated how much of the underlying technology supply chain flows through Asia regardless of where the robot is assembled.

What the Market Actually Looks Like — and When

Strip away the most optimistic projections and a clearer picture emerges. Morgan Stanley's updated forecast estimates the humanoid market at roughly $200,000 per unit today, declining to about $150,000 by 2028 and $50,000 by 2050. At $200,000 per unit, the addressable market is industrial customers with very specific, high-value applications that justify the capital outlay and the operational overhead. That's a real market — but it's not the "robot in every warehouse" scenario the funding headlines imply.

The household market, despite consumer excitement, remains a distant prospect. Morgan Stanley projects only 80 million units in homes by 2050, compared to 930 million in industrial and commercial use. Widespread home adoption requires prices below $50,000 and a level of dexterity and reliability that the industry's own experts say will require "another decade" of hardware and AI model development.

The companies that will survive this shakeout are likely the ones that resist the temptation to overpromise on timeline and instead focus on demonstrating genuine reliability in narrow, high-value industrial tasks. Mind Robotics raised $500 million in March 2026 betting that the right industrial AI doesn't need a human body at all — which is, if nothing else, a coherent response to the form factor risk. Meanwhile, safety researchers have grown increasingly vocal about consumer deployment timelines that outpace the available safety evidence.

The Reckoning Arrives Gradually, Then Suddenly

The humanoid robotics industry is not fraudulent. The underlying technology is advancing, the applications are real, and the long-term market opportunity is substantial. But the gap between where the industry is today and what it publicly committed to for 2026 is going to become visible over the next three quarters — in missed production targets, delayed customer deployments, and the quiet replacement of "50,000 units" language with more carefully hedged forward guidance.

That's not a disaster. Industrial deeptech development consistently runs on longer timelines than public projections. The question is whether the capital markets, having priced in the aggressive scenario, will give these companies the runway to deliver on the realistic one. NVIDIA's physical AI platform, unveiled at GTC 2026 in March, is real infrastructure for the robot era — but even Jensen Huang's framing distinguished between what's being deployed now and what the platform is designed for eventually.

Fifty thousand Optimus robots by December 2026 would be a manufacturing miracle. Fifty thousand by the end of 2027 would be a serious business. The industry's credibility — and much of its available capital — depends on which of those timelines turns out to be accurate.